Maximizing Your Retirement Savings on a Low Income

Planning for retirement can feel daunting, especially if you’re working with a tight budget. The good news is that even with limited resources, you can still build a solid nest egg by making smart decisions about where and how to save. This post will guide you through various retirement savings options, offer strategies for increasing your savings, and help you avoid common pitfalls.

Understanding Your Retirement Savings Options

When it comes to saving for retirement, the type of account you choose matters. Different accounts offer various benefits, from tax advantages to employer contributions, and understanding these can help you make the most of every dollar you save.

Employer-Sponsored Plans: Start with the Match

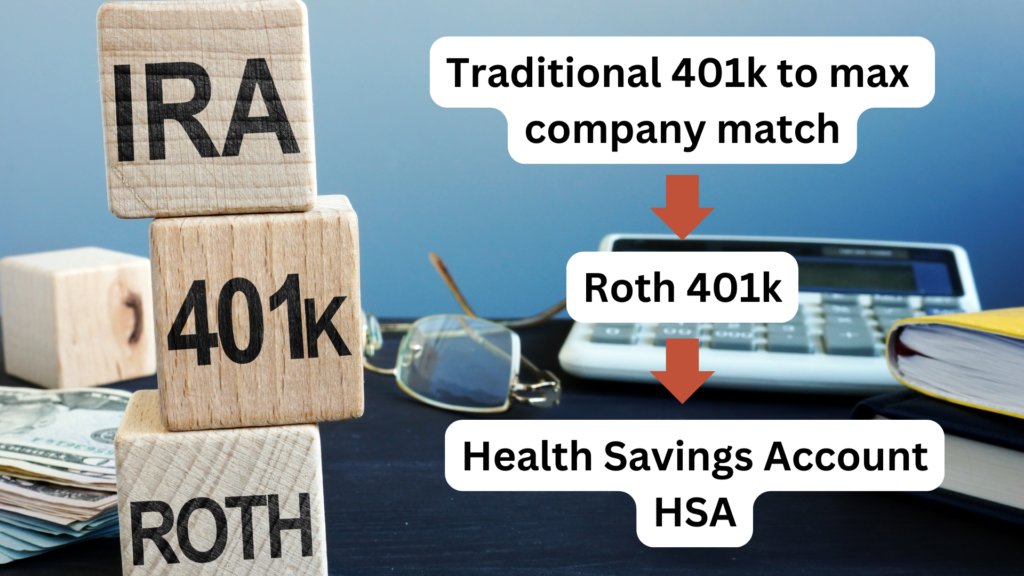

If your employer offers a retirement savings plan, such as a 401(k), with a matching contribution, this should be your first stop. An employer match is essentially free money—by contributing a percentage of your salary, your employer will match that amount up to a certain limit. For example, if your employer matches 50% of your contributions up to 6% of your salary, you should aim to contribute at least 6% to take full advantage of the match.

Why Start Here?

The match not only boosts your savings but also offers immediate returns on your contributions, making it one of the most powerful tools for building your retirement fund.

Roth IRA: Tax-Free Growth

After maximizing your employer match, the next step is to consider a Roth IRA. A Roth IRA is a retirement account where you contribute after-tax dollars, and in return, your investments grow tax-free. When you withdraw the money in retirement, you won’t owe any taxes on it, provided you meet the conditions.

Advantages of a Roth IRA:

- Tax-Free Withdrawals: Since you’ve already paid taxes on the money you contribute, withdrawals in retirement are tax-free. This is particularly beneficial if you expect to be in a higher tax bracket in the future.

- Flexibility: Roth IRAs offer more flexibility than other retirement accounts. For example, you can withdraw your contributions (but not earnings) at any time without penalties or taxes.

A Roth IRA is particularly advantageous for those on a low income who expect their tax rates to be higher in retirement, making the tax-free withdrawals even more valuable.

Traditional IRA: Tax-Deferred Growth

If you’ve maxed out your Roth IRA contributions, the next option is a Traditional IRA. Contributions to a Traditional IRA are typically tax-deductible, meaning you can reduce your taxable income in the year you contribute. The investments grow tax-deferred, and you’ll pay taxes when you withdraw the money in retirement.

Advantages of a Traditional IRA:

- Tax Deduction Now: Reducing your taxable income today can be beneficial if you’re in a higher tax bracket now than you expect to be in retirement.

- Potential for Lower Taxes Later: If you expect to be in a lower tax bracket during retirement, a Traditional IRA can help you save on taxes when you begin withdrawing funds.

Prioritizing Retirement Savings on a Tight Budget

Saving for retirement on a low income requires careful budgeting and disciplined saving habits. Here are some strategies to help you prioritize your retirement savings, even when money is tight.

Budgeting for Savings

The first step is to create a budget that allocates a portion of your income to retirement savings. Start by tracking your income and expenses to see where your money is going. Once you have a clear picture of your financial situation, look for areas where you can cut back.

Tips for Budgeting:

- Automate Your Contributions: Set up automatic transfers to your retirement accounts. This way, you won’t be tempted to spend the money before you save it.

- Cut Non-Essential Expenses: Review your spending and identify non-essential expenses that can be reduced or eliminated. For example, consider cooking at home more often instead of dining out.

- Set Savings Goals: Define specific savings goals for your retirement accounts. For instance, aim to contribute a certain percentage of your income each year.

Start Small, Think Big

If you’re just starting out and can’t afford to contribute much, that’s okay. The key is to start saving whatever you can, even if it’s just a small amount. Over time, you can increase your contributions as your income grows or as you find additional ways to save.

Example Strategy:

- Start with 1%: Begin by contributing 1% of your income to your retirement accounts. After a few months, try increasing it to 2%, then 3%, and so on. Small, consistent increases can add up over time.

Employer Matches: Don’t Leave Free Money on the Table

As mentioned earlier, always aim to contribute enough to your employer-sponsored plan to take full advantage of any matching contributions. This is one of the easiest ways to boost your retirement savings.

Strategies for Increasing Retirement Savings

Beyond budgeting and employer matches, there are other strategies you can use to increase your retirement savings.

Side Hustles and Extra Income

Consider taking on a side hustle or part-time job to generate extra income. This additional income can be dedicated entirely to your retirement savings, accelerating your progress.

Examples of Side Hustles:

- Freelance Work: Offer your skills as a freelancer in areas like writing, graphic design, or programming.

- Gig Economy Jobs: Participate in gig economy jobs such as ridesharing, food delivery, or dog walking.

- Selling Unused Items: Sell items you no longer need on platforms like eBay or Facebook Marketplace.

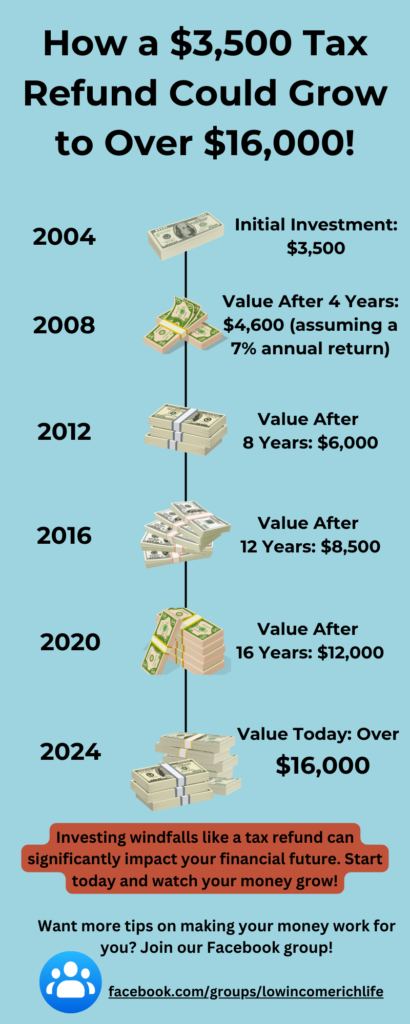

Windfalls and Bonuses

If you receive unexpected windfalls—such as tax refunds, bonuses, or gifts—consider putting a portion of that money into your retirement savings.

Example Strategy:

- 50/50 Rule: When you receive a windfall, put 50% into your retirement savings and use the other 50% for something else, like paying down debt or treating yourself.

Downsizing and Simplifying

Another way to free up more money for retirement is to simplify your lifestyle. This could mean downsizing your home, reducing your transportation costs, or cutting back on luxury expenses.

Examples of Downsizing:

- Move to a Smaller Home: Consider moving to a smaller, more affordable home or apartment to reduce housing costs. (Check out our post -> Housing Options For A Low Income Retirement.

- Reduce Vehicle Costs: If you have multiple vehicles, consider selling one and using public transportation or carpooling to save on maintenance, insurance, and fuel.

Health Savings Accounts (HSAs) vs. Flexible Spending Accounts (FSAs)

An often overlooked retirement savings tool is the Health Savings Account (HSA). HSAs offer unique tax advantages and can be a powerful way to save for medical expenses in retirement.

Health Savings Accounts (HSAs)

HSAs are tax-advantaged savings accounts available to individuals with high-deductible health plans (HDHPs). Contributions to an HSA are tax-deductible, the funds grow tax-free, and withdrawals for qualified medical expenses are also tax-free.

Why HSAs are Great for Retirement:

- Triple Tax Advantage: HSAs offer a triple tax advantage—tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

- Roll Over Unused Funds: Unlike FSAs, unused funds in an HSA roll over year after year, allowing your balance to grow over time.

- Use for Any Purpose After Age 65: After age 65, you can use HSA funds for non-medical expenses without penalty (though you will owe taxes on non-medical withdrawals).

Flexible Spending Accounts (FSAs)

FSAs are another type of tax-advantaged account used to pay for medical expenses. However, they differ from HSAs in several key ways.

Key Differences Between HSAs and FSAs:

- Use It or Lose It: Unlike HSAs, FSAs typically require you to use the funds within the plan year or risk losing them, although some plans offer a grace period or allow a small portion to roll over.

- No Investment Growth: FSA funds do not earn interest or grow over time, making them less advantageous for long-term savings compared to HSAs.

- Limited Portability: FSAs are often tied to your employer, meaning you could lose access to your funds if you change jobs.

Common Pitfalls to Avoid

As you work towards building your retirement savings, be mindful of these common pitfalls that can derail your progress.

Cashing Out Early

One of the biggest mistakes people make is cashing out their retirement savings early. This often results in penalties, taxes, and a significant reduction in your retirement nest egg.

How to Avoid This:

- Consider a Rollover: If you change jobs, consider rolling over your 401(k) into an IRA instead of cashing it out.

- Emergency Fund: Build an emergency fund separate from your retirement savings to avoid the temptation to dip into your retirement accounts.

Over-Reliance on Social Security

While Social Security can be an important part of your retirement income, it’s unlikely to be enough to cover all your expenses. Relying too heavily on Social Security can leave you vulnerable to financial shortfalls in retirement.

Strategy:

- Supplement with Savings: Ensure that you’re building additional savings through IRAs, 401(k)s, or other investment accounts to supplement Social Security.

Neglecting to Adjust Savings Over Time

As your income increases or your financial situation changes, it’s important to adjust your retirement contributions accordingly.

Example Strategy:

- Annual Review: Make it a habit to review and adjust your retirement contributions every year, especially after receiving a raise or paying off debt.

Conclusion:

Building a secure retirement on a low income is challenging, but with careful planning and smart strategies, it’s entirely possible. By understanding your retirement savings options and prioritizing your contributions—starting with employer matches, followed by Roth IRAs, and then Traditional IRAs—you can maximize your savings potential. Don’t forget to leverage Health Savings Accounts (HSAs) for their triple tax advantages, and be mindful of common pitfalls like cashing out early or relying too heavily on Social Security.

Remember, the key to successful retirement planning is to start early, save consistently, and regularly review your progress. Even small steps can lead to significant growth over time. Use the strategies outlined in this post to take control of your financial future and work towards a retirement that provides peace of mind and financial security.

Call to Action: Take the first step today by reviewing your current retirement savings plan. If you haven’t already, set up automatic contributions, explore additional income opportunities, or consider downsizing to boost your savings. And don’t forget to check out our Facebook Group for more exclusive tips and strategies to save and prepare for retirement on a low income.